Vietnam’s confectionery market—worth nearly USD 1.8 billion and growing at over 6.8% annually—is heating up as global players double down on expansion while local brands scramble to stay in the game.

The recent acquisition of Bibica by Indonesia's Sari Murni Abadi (SMA) has drawn attention across Southeast Asia. More than just a business deal, it signals an intensifying race for dominance in Vietnam’s high-growth snack and confectionery market.

According to SMA CFO Mr. Servin, the acquisition aligns with the company’s global expansion roadmap, aiming to strengthen its role as a key FMCG producer and distributor. SMA’s move also allows for product line diversification—from snacks to biscuits and sweets—while integrating supply chains and accelerating innovation.

Already known for the Momogi brand in Indonesia, SMA has been expanding rapidly into markets like South Korea, the Middle East, and now Vietnam. Through Bibica’s 100,000+ distribution points, strong local presence, and export capabilities, SMA is positioning itself to scale across Southeast Asia.

Meanwhile, Korean food giant Orion recently broke ground on its third factory in Vietnam—Yen Phong 2C Industrial Park, Bac Ninh. The plant is set to boost Orion’s production capacity and solidify Vietnam as its strategic manufacturing base in Southeast Asia.

Mondelez Kinh Do Vietnam has also appointed a new General Director to usher in its next growth phase. Mondelez’s acquisition of Kinh Do’s confectionery business for USD 570 million in 2014 enabled it to develop dozens of popular brands for Vietnamese consumers.

Philippines-based Liwayway Holdings, owner of the Oishi brand, has steadily grown its market share since 1997, leveraging school canteens and retail networks to reach even rural areas.

According to Statista, Vietnam’s confectionery market is expected to grow at a CAGR of 6.81% from 2025–2030. Economic growth, rising incomes, and evolving consumer tastes—especially for premium snacks—are fueling the demand.

Cốc Cốc’s 2025 industry report echoes these findings, noting that foreign companies dominate the market with brands like Oshi (Liwayway), Lay’s (Pepsico), Nestlé, and Lotte. These firms are investing aggressively, indicating confidence in long-term opportunities.

As foreign players scale up, Vietnamese brands are under pressure to differentiate. Many are upgrading packaging, diversifying offerings, and adapting to new consumer demands—especially health-conscious choices.

A Cốc Cốc survey reveals that 4 out of 5 Vietnamese consumers now look for snacks that are low-sugar, preservative-free, or made with natural ingredients—up 3% from 2024.

Young consumers (13–24) prioritize taste and price, while those 25+ focus more on nutrition and origin. Brands must respond to both groups with tailored products and messaging.

Seasonal launches—especially around Tet and Mid-Autumn—offer ideal windows to test limited editions and premium offerings.

The gap between agile and stagnant companies is becoming clear:

In short, those investing in production tech, branding, and innovation are gaining ground. Those lagging behind risk being left out of the high-stakes battle for Vietnam’s snack shelves.

Vietnam’s merchandise trade is set to reach a new milestone in 2025, with total export–import turnover estimated at USD 920 billion, up 16.9% year on year. The country is expected to post a trade surplus of USD 21.18 billion, marking the 10th consecutive year of surplus.

Monday, 29 Dec, 2025

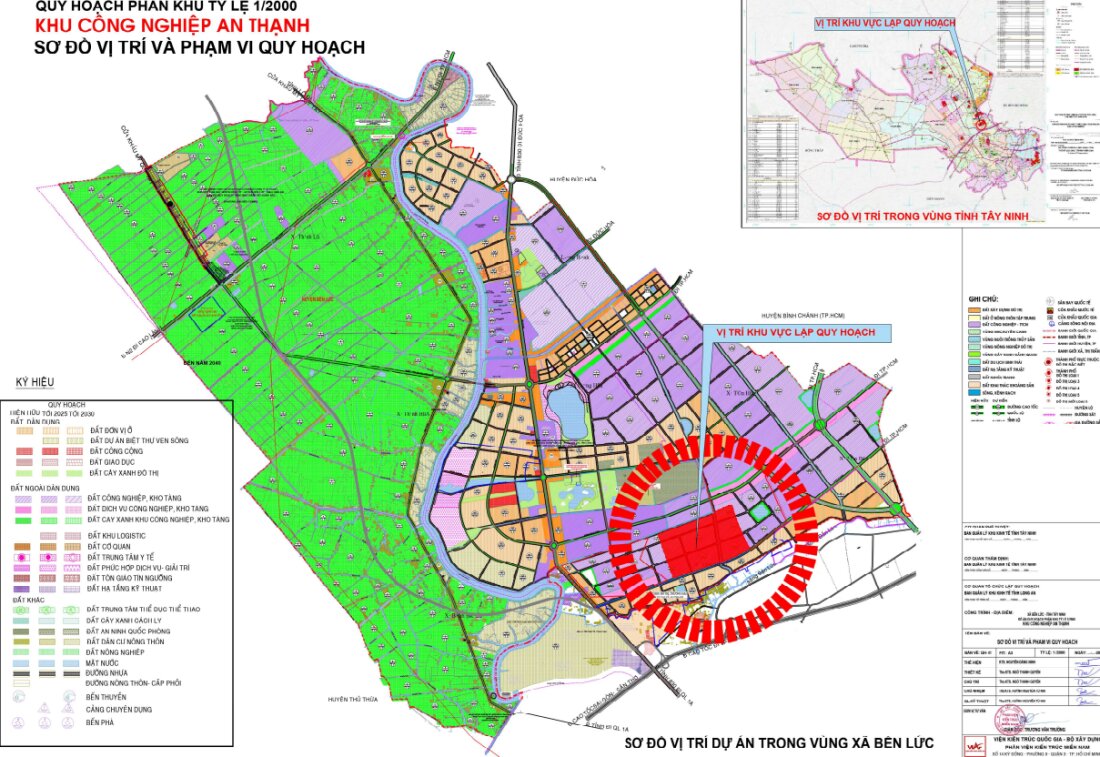

Tay Ninh has approved An Thanh Industrial Park Phase 1 under Decision No. 5820/QĐ-UBND dated April 6, 2026. The 264.3-hectare project in Ben Luc commune has more than VND4.795 trillion in investment and is oriented toward green, high-tech, multi-sector industrial development.

Friday, 24 Apr, 2026

Victory Giant Technology’s Vietnam revenue reached about USD 473 million in 2025, equal to 16.8% of total group revenue. The growth reflects Vietnam’s rising role in PCB manufacturing, supported by a USD 520 million factory project and demand from AI, data center and high-performance computing applications.

Wednesday, 22 Apr, 2026

Hòa Phát Refrigeration plans to invest USD 50 million in a new refrigerator factory in Phú Mỹ, Ho Chi Minh City, with annual capacity of 1.2 million products. The factory will produce large-capacity refrigerators for Vietnam and export markets including North America, Europe and parts of Asia.

Tuesday, 05 May, 2026

Big trade numbers alone no longer guarantee sustainable growth. The real challenge for Vietnam is turning strategic messages into clear, executable actions that improve value retention, resilience, and long-term competitiveness.

Monday, 29 Dec, 2025

The go-to platform for Expert Voices. Get to know more about the people behind the business. Book to meet with the right experts for your business needs.

Service detailThe go-to Community for Industrial growth. Meet, interact, showcase and find opportunities with professionals across different industries, across borders.

Service detail